Everything about How Many Mortgages To Apply For

Considering the limitations imposed upon HECM loans, they are comparable to their "Forward" contemporaries in overall expenses. The following are the most common closing expenses paid at closing to get a reverse home mortgage: Therapy charge: The initial step to get a reverse home loan is to go through a therapy session with a HUD-approved counselor.

Origination cost: This is charged by the lending institution to organize the reverse mortgage. Origination costs can differ widely from lending institution to loan provider and can vary from nothing to an optimum of $6,000. Third-party fees: These costs are for third-party services worked with to complete the reverse mortgage, such as appraisal, title insurance coverage, escrow, federal government recording, tax stamps (where relevant), credit reports, and so on. how do reverse mortgages work in california.

The IMIP protects lending institutions by making them whole if the house costs the time of loan repayment for less than what is owed on the reverse home loan. This secures debtors as well because it means they will never ever owe more than their home is worth. As of 1/2019, the IMIP is now 2% of limit claim quantity (Either the evaluated worth of the house up to an optimum of $726,535) The yearly MIP (home loan insurance coverage premium) is.

Getting The How Do Interest Rates On Mortgages Work To Work

The huge bulk of closing costs usually can be rolled into the brand-new loan quantity (other than when it comes to HECM for purchase, where they're included in the down payment), so they don't need to be paid of pocket by the borrower. The only exceptions to this rule might be the therapy cost, appraisal, and any repairs that may need to be done to the home to make it completely certified with the FHA standards before finishing the reverse home loan.

These files can be used to compare loan deals from various lenders. There are 2 ongoing expenses that might use to a reverse mortgage: yearly mortgage insurance coverage and servicing charges. The IMIP,(on time Initial Mortgage Insurance Premium) of 2% of the evaluated value is charged at closing. The IMIP is the largest expense connected with an FHA HECM or Reverse Home Loan. The credit line just accumulates interest on the amount you access when you access it. If you need a combination of some cash upfront, extra earnings and a line of credit to access, a reverse home loan has the versatility to provide all of these. Make certain you comprehend how each element works prior to you sign your closing documents.

The equity in your home is reduced every month you have a reverse mortgage balance outstanding.: If you prepare to leave your property to your household, there will be less equity for them as the reverse home loan balance grows (how do mortgages payments work).: If you get Medicaid or Supplemental Security Income (SSI), ensure you discuss the effect reverse mortgage earnings could have on the future invoice of this earnings.

Some Known Incorrect Statements About How Do Mortgages And Down Payments http://dearusutkw.nation2.com/some-known-incorrect-statements-about-how-is-fredd Work

The HECM origination fee maximum is $6,000. The upfront costs are flexible, so look around to make sure the charges you are being charged are affordable. After you close a reverse mortgage, you require to be knowledgeable about how the loan provider will remain in touch with you. There are some essential things you'll require to interact to your lender if your health or housing needs alter.

Each year your servicer will send you a Yearly Occupancy Certification to validate you live there. If you forget to send it, you may get a check out from an inspector to confirm you are still living there. If they aren't able to verify that, your lending institution might consider you in default of your reverse home loan.

They might need that you utilize some of your reverse home loan funds to pay any delinquent home expenditures. Your lender needs to be alerted instantly if anyone who obtained the reverse home loan passes away. In many cases, an enduring partner will be allowed to remain in the residential or commercial property, however there might be extra requirements if the enduring spouse was not on the original reverse home mortgage.

How How Adjustable Rate Mortgages Work can Save You Time, Stress, and Money.

Here are a few of the most common reverse home loan scams and how to avoid them. You must never borrow money to take into "investment programs." Although in many cases this may be more dishonest than illegal, unethical monetary organizers may attempt to persuade you to take the cash out to buy the market.

This often involves a knock on the door by somebody representing themselves as a friendly area handyman, with suggestions for work that they can do on the house. Ultimately, other specialists might begin to suggest costly repairs that might or may not require to be done, and after that advise funding them with a reverse home loan.

Only look for relied on repair services from a licensed contractor. If a relative suddenly and persistently begins asking about your monetary condition, and suggests a power of attorney integrated with a reverse home loan, this could be an indication of inheritance fraud. There are companies that can assist if you think you are or a relative is a victim of any kind of elder abuse.

![]()

Some Known Questions About How Do here Mortgages Work Condos.

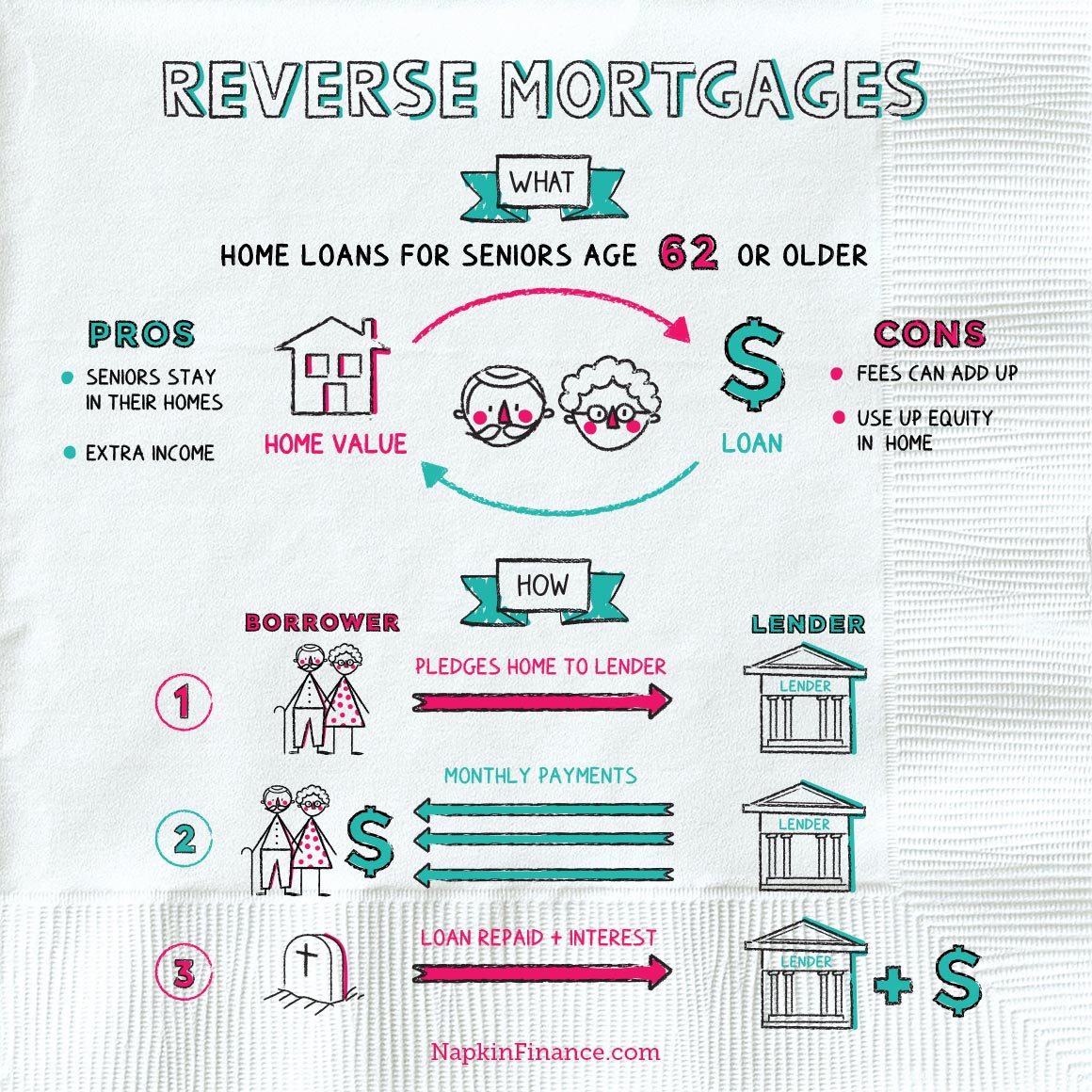

A reverse mortgage is a loan readily available to house owners, 62 years or older, that allows them to convert part timeshare cancellation companies of the equity in their houses into money. The item was conceived as a method to help senior citizens with restricted income utilize the built up wealth in their houses to cover standard month-to-month living expenses and spend for healthcare.

The loan is called a reverse home mortgage because instead of making monthly payments to a lender, just like a traditional home mortgage, the loan provider makes payments to the customer. The customer is not needed to repay the loan up until the house is sold or otherwise left. As long as the borrower resides in the house he or she is not needed to make any monthly payments towards the loan balance.

Chances are, you have actually seen commercials boasting the benefits of a reverse mortgage: "Let your home pay you a regular monthly dream retirement income!" Sounds great, ideal? These claims make a reverse mortgage noise nearly too good to be real for senior homeowners. But are they? Let's take a better look. A reverse mortgage is a type of loan that uses your home equity to supply the funds for the loan itself.

7 Easy Facts About How Do Reverse Mortgages Work Example Explained

It's generally an opportunity for retired people to tap into the equity they've built up over many years of paying their mortgage and turn it into a loan for themselves. A reverse home loan works like a regular home loan in that you have to use and get authorized for it by a lender.

However with a reverse mortgage, you do not make payments on your home's principal like you would with a routine mortgageyou take payments from the equity you have actually built. You see, the bank is providing you back the cash you have actually already paid on your house but charging you interest at the very same time.